We propose increasing the average Work levy rate for employers and self-employed from $0.63 to $0.66 per $100 of payroll for 2025/26, increasing this to $0.69 in 2026/27, and $0.72 in 2027/28.

| Work Account | Current (2024/25) | 2025/26 | 2026/27 | 2026/27 |

| Cost of supporting recovery | $1,407,094,228 | $1,517,648,082 | $1,595,219,199 | |

| Operating costs | $59,202,594 | $59,276,210 | $60,557,651 | |

| Total funding for new claims | $1,466,296,822 | $1,576,924,292 | $1,655,776,850 | |

| Funding adjustment for current funding position | -$185,964,594 | -$183,540,438 | -$167,957,741 | |

| Levy required for the year | $1,280,332,229 | $1,393,383,854 | $1,487,819,108 | |

| Accepted funding shortfall from FPS caps | -$210,687,582 | -$220,902,318 | -$212,545,587 | |

| Proposed levy | $1,069,644,647 | $1,172,481,536 | $1,275,273,522 | |

| Work levy per $100 liable earnings | $0.63 | $0.66 | $0.69 | $0.72 |

| Year on year change | +4.8% | +4.5% | +4.3% |

The recommended Work Account levies are 27% ($397 million) lower than the full cost of supporting the new injuries we expect in 2025/26.

Setting levies for individual businesses

ACC uses insurance industry practices such as risk rating to create levy rates that reflect a business’ claim risk. We apply an industry standard approach to create groups of businesses that have similar characteristics in terms of work undertaken, injury frequency, and cost of recovery. The diversity of work across New Zealand has led us to create 142 groups of businesses we call levy risk groups. Each group meets a size threshold that helps to keep levies stable over time while also ensuring that there is recognition of differences between industries (sectors) and the different types of work in each industry.

A simpler system with fewer groups would create more stability in levies but would mean the businesses in each group would be less similar and there would be more cross-subsidisation between businesses in each group.

To make it easier for a business to identify which group it belongs to, ACC has developed 537 classification units and 2,500 business industry classification codes which describe the activity of businesses in a more detailed way.

The business industry classification codes map to classification units which are linked to the levy risk group. ACC sets the levy rates for businesses at the levy risk group level and publishes these rates alongside the classification units in the levy regulations.

We’re recommending that the aggregate Work levy is increased to the maximum allowable under the Funding Policy Statement each year for the next three years.

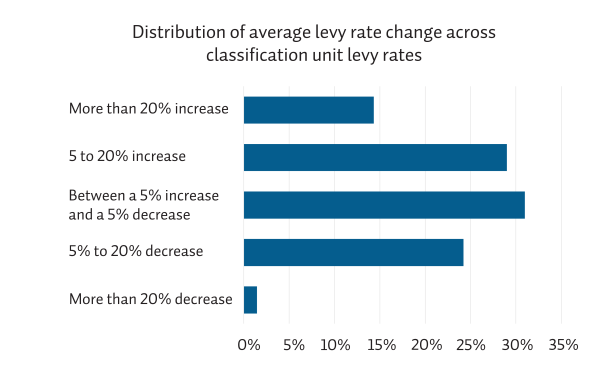

Levy rates for each classification unit are updated to reflect any changes in their claims patterns.

This will mean levy rates for some businesses will increase when the average rate is decreasing or decrease when the average rate is increasing.

The Working Safer Levy

We also collect the Working Safer Levy on behalf of the Ministry of Business, Innovation and Employment (MBIE) for supporting WorkSafe’s enforcement, education and engagement activities across the country.

This is currently a flat rate of $0.08 per $100 of liable earnings and is not part of this consultation

Reasons behind proposed increase

There are historic funding surpluses in the Work Account. We have been able to use these surpluses to keep levies below the full cost of claims for the last 10 years. If the proposed levy rates are agreed by Government, levy rates for the next three years will remain as much as 46% below the cost of injuries for the different levied Accounts.

As the surpluses are used up, and the volumes of claims continue to grow, levies will still need to be increased to cover the full costs of claims.

Between June 2021 and June 2024, the number of claims, the number of claims for injuries that require time off work to recover has grown by 7%.

Compared to the last levy consultation in 2021, the costs of injuries for the 2025/26-2027/28 levy years are expected to be higher due to an increase in the:

- Numbers of injuries requiring time off work.

- Costs for funding of ambulance and public health acute services (PHAS).

- Recovery time required before the worker can return to work.

- Number and cost of sensitive claims in the Earners’ Account (mental injury caused by sexual violence).

- Inflationary pressures in the past three years.

Sole trader

What you are currently paying:Industry: {{ userInput.bic.text }}

Structure: Sole trader

Projected income: {{ userInput.structure.soleTrader.amountParsed | dollarize }}

While we’re recommending that the average Work levy is increased each year over the next three years, levy rates for each CU are also updated to reflect any changes in their claims patterns. This means levy rates for some businesses will increase above the proposed increase to the average rate, and decrease for other businesses.

These results are estimates based on the proposed levy rates and will be subject to Cabinet's final decisions and any changes in your liable earnings each year.

The Minister for ACC is also consulting on changes to specific CUs for professional sports and large home improvement stores, which are not reflected in these estimates.

Shareholder

What you are currently paying:Industry: {{ userInput.bic.text }}

Structure: Shareholder employee

Projected income: {{ userInput.structure.shareholderEmployee.totalAmountNotCapped | dollarize }}

While we’re recommending that the average Work levy is increased each year over the next three years, levy rates for each CU are also updated to reflect any changes in their claims patterns. This means levy rates for some businesses will increase above the proposed increase to the average rate, and decrease for other businesses.

These results are estimates based on the proposed levy rates and will be subject to Cabinet's final decisions and any changes in your liable earnings each year.

The Minister for ACC is also consulting on changes to specific CUs for professional sports and large home improvement stores, which are not reflected in these estimates.

Employer

What you are currently paying:Industry: {{ userInput.bic.text }}

Structure: Employer

Projected income: {{ userInput.structure.employer.amountParsed | dollarize }}

While we’re recommending that the average Work levy is increased each year over the next three years, levy rates for each CU are also updated to reflect any changes in their claims patterns. This means levy rates for some businesses will increase above the proposed increase to the average rate, and decrease for other businesses.

These results are estimates based on the proposed levy rates and will be subject to Cabinet's final decisions and any changes in your liable earnings each year.

The Minister for ACC is also consulting on changes to specific CUs for professional sports and large home improvement stores, which are not reflected in these estimates.